Longevity reinsurance is booming in the Netherlands. What are the drivers and will the rest of Europe follow suit?

What occupation should you pursue if you want to live longest? According to the panel on longevity at Life-Re Europe, librarian might be a good bet. That was the occupation of Prudential Financial’s oldest living pension risk transfer (PRT) annuitant, who started receiving payments from the insurer way back in 1929, when the insurer transacted what it calls the first pension buy-out contract of its kind – and the start of its PRT business – with the Cleveland public library.

The librarian in question has no doubt retired now, however longevity continues to occupy the minds of insurers and pension plans around the world.

At Life-Re Europe, a longevity panel debated the recent boom in PRT and longevity risk transfer in Europe – or more specifically in the Dutch market, which has seen a sizeable number of local companies enter the PRT business and offload unwanted pensions to insurers on the back of its Dutch pension reform in 2023.

Going Dutch

Panellists at Life-Re Europe included from Pacific Life Re and a.s.r. NL, which transacted a €1.3 billion longevity swap in February this year, as well as NN and Prudential, which together did a €4 billion longevity risk transfer in 2025.

The other Dutch insurer on the panel, asr, has done three transactions in total.

“A big driver has been reducing concentration on the balance sheet,” said Jouke Hottinga, Managing Director, Group Strategy & Balance Sheet Management, a.s.r. NL. “We had also tried to reduce longevity risk in the past using index swaps. That was ineffective from a capital perspective because of all the basis risk from the index. So we looked at more effective ways to reduce risk.”

Efficacy aside, carrying out a longevity deal can still be challenging from an operational perspective. Data issues have been tricky, particularly on the pensions side.

“When we were first going into the Dutch pension market, processes were a bit clunkier, the data wasn’t as great,” according to Rohit Mathur, Head of International Reinsurance Business at Prudential Financial. “The buyout advisors were still climbing the learning curve. Which are all things you would see in a newer market. But when you go to insurers, data is much better. Insurers have to get their reserves right, pension plans less so.”

While the Dutch PRT volumes have not been as big as initial €20 to €30 billion predictions, as pension funds have looked at other options like consolidation, participants remain positive on future prospects for the Dutch longevity risk transfer market.

“The transition is not over yet – there are a couple more years until it’s complete, so we will see more volumes materialising over time,” said Emily Eskandari, Assistant Vice President, Client Solutions, Continental Europe, Pacific Life Re.

Eskandari said it was not clear what type of insured solutions will be pursued given differences between a flexible premium regime, where individuals will have to choose between a fixed annuity or a variable annuity, and a solidarity premium regime, where it will be more of a collective approach.

“But ultimately there still is longevity risk remaining with those schemes,” she added. “So the market is still evolving, and we do expect that there will be a bigger market to come, just in a more alternative and evolved state than it currently is from a traditional PRT approach.”

Beyond the Netherlands

But what about the rest of Europe? Wider Europe has not had a catalyst to drive PRT, as seen in the Netherlands’ pension reforms.

Panellists said there have been transactions in Belgium and Switzerland, and discussions in other markets like Germany and Iberia, but nothing concrete has emerged to point to one country being the next big market. Potential drivers, from the reinsurance side, are likely to be availability of data, and a landmark longevity reinsurance transaction to establish a model for the market.

“We will need to see whether a market can come forward with adequate amount of data for a reinsurer to be able to price liabilities,” said Eskandari. “We need to be able to understand the underlying products, the underlying population, and really be able to construct the basis and get comfortable in a country that we may not fully understand.”

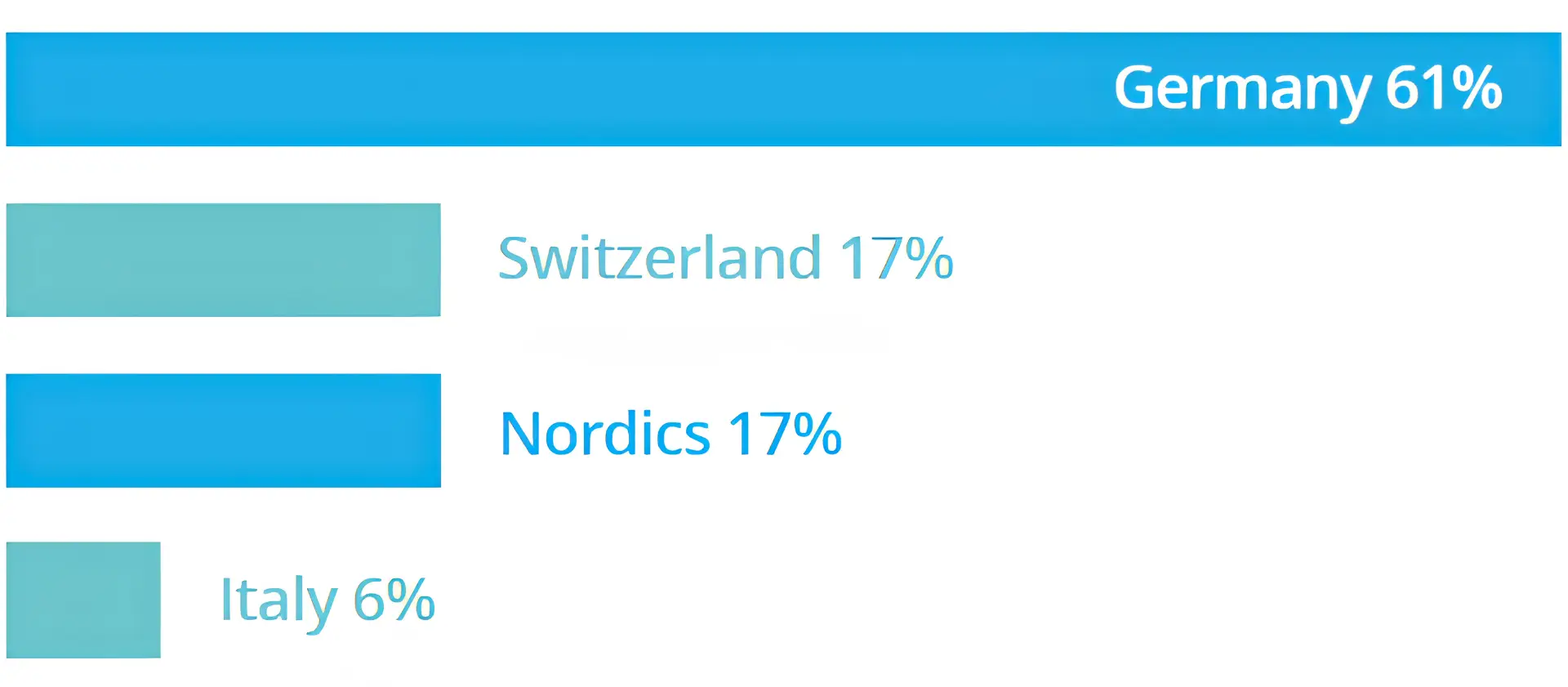

And having a precedent deal is all important to highlight regulatory comfort. It remains to be seen who will go first – though Life-Re audience members plumped for Germany.

Life-Re Poll

Which of these countries will have active pension/ longevity risk transfer markets within the next five years?

Source: Life-Re Europe audience poll.